Don't Blame Biden for Inflation: Part 2

Don't Blame Biden for Inflation: Part 2

Inflation is a global phenomenon

The case against Biden on inflation is simple. Early in 2021, shortly after Biden took office, he proposed (and Congress passed in bipartisan fashion) a massive COVID stimulus of nearly $2 trillion dollars, the American Rescue Plan (ARP). Inflation spiked shortly thereafter, and has only recently come back down. That all happened.

But did inflation go up in 2021 because of the ARP? The case looks open and shut. The ARP was a positive demand shock, and those cause inflation. So we’d expect to see a huge spike in inflation in the US in 2021 as a result, and that’s what happened. Yet if the ARP was the cause of the inflation we saw in the US, then we wouldn’t expect to see similar spikes in inflation in the rest of the world. After all, the American Rescue Plan was an American rescue plan. But here’s what global inflation looked like in the early 2020s:

Huh.

Those graphs cover different time periods - the graph of global inflation goes back to 2010, not just to 2019. But if you look at the period from 2019 to today in both graphs, you see something striking: Modest, 2%ish inflation in 2019 and before. A sharp drop in inflation in early 2020 with the onset of COVID. That lowered inflation bumbles along for 2020, and then inflation shoots through the roof all over the world, including in the US, in early 2021. That spike in inflation peaked in mid-2022, then started to head down. That happened everywhere. So that spike in inflation was not plausibly caused by the ARP. That would explain the high US inflation, but it wouldn’t explain high global inflation.

And that’s the case for exonerating Biden in a nutshell: the case against him is that inflation spiked after the ARP, which he championed. But it’s not plausible that inflation spiked BECUASE of the ARP, since the inflation spike was a global phenomenon. And the US under Biden doesn’t have worse inflation than the rest of the world today. Global inflation is around 4% today, and in the OECD it’s at 6%. In the US, it’s around 3%. We’re not at the head of the pack in terms of fighting off inflation, but we’re much better than average:

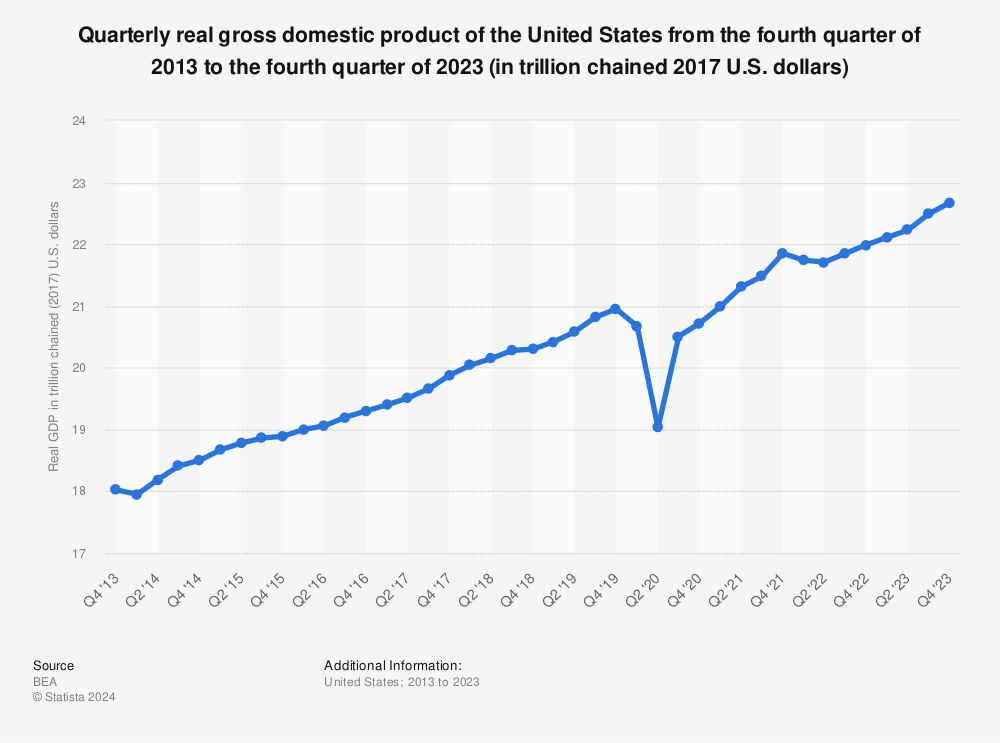

So Biden didn’t cause inflation. What did, though? Well, COVID. Obviously. (The invasion of Ukraine in early 2022 probably kept things pushing up for a few more months as well.) But here things get a bit tricky to tease out. Because COVID happened in early 2020, and that corresponded to a drop in inflation. And it also corresponded to a massive drop in GDP:

We’ve now got all of the pieces of our puzzle. Time to put them together.

In Part 1, I talked about three kinds of “shocks” to the economy, negative supply shocks, negative demand shocks, and positive demand shocks. A negative supply shock leads to lower GDP and high inflation. A negative demand shock leads to lower GDP and lower inflation. A positive demand shock leads to higher GDP and higher inflation. So it seems pretty clear that COVID in 2020 corresponded to a sharply negative demand shock to the economy. (People were buying less, because they were staying at home all day every day.) Inflation fell, as did GDP.

But then in 2021, the global economy experienced a second shock: a negative SUPPLY shock. This was also an effect of COVID (although, as in the 1970s, the negative supply shock also corresponded with a sharp increase in oil prices, and that probably played a role, too). Why was the negative supply shock from COVID delayed by a year, relative to the negative demand shock? That’s a good question, but the answer appears to be, roughly, “supply chains.” Manufacturing and shipping of goods was massively disrupted by COVID. That didn’t matter much so long as businesses had inventory that they could sell down. But as inventories got sold down and businesses had to start selling goods that had been manufactured more recently, there were just fewer goods around to sell because of the huge disruptions to both manufacturing and shipping that were making headlines in 2021. So (at any given price level) businesses were able to sell fewer goods. That’s the definition of a negative supply shock. Negative supply shocks lead to inflation, and so we got plenty of inflation in 2021.

But did the ARP make things worse? After all, stimulus, like the ARP, constitutes a positive demand shock. Those cause higher inflation and higher GDP. So did the ARP make inflation higher than it otherwise would have been? Sure, I guess. Probably. But at this point it’s important to consider effect sizes. Positive demand shocks make inflation worse, but HOW MUCH worse?

Here are two data points. First: Global inflation spiked up to just below 9% in 2022. US inflation spiked up to just above 9% in 2022. So perhaps the ARP added about half a percent to inflation during that time. It likely made things worse, but not by a lot.

Second: Look at what happened during the global financial crisis. There was a massive recession that resulted from a negative demand shock. The Fed set rates to 0%, maxing out the positive demand shock possible from monetary policy. The Obama administration wanted to do fiscal stimulus to add to that positive demand shock. But conservatives screamed in protest. The Wall Street Journal ran a new editorial every day warning that stimulus leads to inflation. So the Obama administration lobbied for, and passed, a stimulus that was substantially smaller than the economists on staff recommended. The result? Years of anemic growth, and sub-1% inflation. The stimulus was inflationary (because all stimulus is inflationary), but it was counteracting deflationary forces, and the net result was not enough growth and not enough inflation.

So with all of this in mind, put yourself in the shoes of the Biden administration in early 2021. The economy has been battered by COVID. Inflation is low because of the negative demand shock, even despite the stimulus passed by Trump. The economy has started to bounce back after an abysmal 2020, but GDP is just back to where it was at the end of 2019; a year and a half of net zero growth. What do you do?

And Biden’s answer was: Go big. In the Obama years, they went small, and it led to years of disappointing economic performance. Go big, and we’ll pull GDP up. Save businesses, so that they don’t have to lay off their employees. Save workers, so they don’t lose their homes. And what about inflation? Well, what about it? In the Obama years, they worried about inflation before it happened, and got years of recession as a result. Interest rates are still at 0%, over a decade later! Go big, and if inflation actually does materialize (the way it failed to in 2009), the Fed can always just raise rates. That’s a perfectly sensible plan. And that’s what they did.

And then supply chain issues (and a spike in global energy prices, and then a war in Ukraine on top) caused a massive negative demand shock, resulting in huge inflation around the world. Inflation took off in the US, like it took off everywhere else. Now it took off more in the US than elsewhere, likely because of the ARP. A rate of 9.1% instead of 8.6% at the top. But that’s hardly the end of the world.

And the plan to save the underlying economy worked fantastically. Economic growth is at all time highs. The stock market is at all time highs. Real wages, particularly for the worst off, are at all time highs. Unemployment is at all-time lows.

The Biden administration made a gamble. In the face of a negative supply shock, they could either stimulate (for higher inflation but better growth) or rein things in (for lower inflation and worse growth). They chose to stimulate, and it worked. Huge boosts to economic growth, with only minimal inflation! And the fact that the US economy was so well-stimulated during that time, and that interest rates were already at 0%, put us in a position to get inflation in check faster and more effectively than most other countries in the world. But the inflation looks massive, because the inflation that the stimulus caused was a bump on top of the massive wave caused by the global negative supply shock from COVID.

Look, hindsight is 20/20. Knowing what we know now about the effects of the ARP on both inflation and growth, I’d be willing — happy, even — to concede that the ARP was a bit too big. If it were $1.6 trillion instead of $1.9 trillion, that might have been closer to ideal. But comparing the performance of the US to other countries around the world, it’s hard to deny that the instinct to go big was the right one, and that the US has navigated the post-COVID inflation better than most countries.

Negative supply shocks are no-win scenarios. But the US has come through the last four years of economic turbulence in better shape than almost any other country in the world. Biden deserves a huge amount of credit for that. Instead, he’s on pace to lose to Donald Fucking Trump. Life’s not fair.

Please, if you find this at all convincing, spread the word. Inflation spiked everywhere in the world 2-3 years ago, approximately as much as it did in the US. That’s not Biden’s fault. It’s just not. Biden’s decision to stimulate into a negative supply shock looks bad, but it resulted in the US having historically high growth and low unemployment. He made difficult but reasonable decisions. And they worked.

Four more years.